We are entering into a third era of enterprise software. Each era has seen a distinct shift of the onus of value delivery away from the customer and onto the vendor. We believe that value capture by AI-native software companies will hinge almost entirely on their ability to continuously deliver exceptional outcomes — making implementations and customer success mission critical.

We see the three eras of enterprise software as:

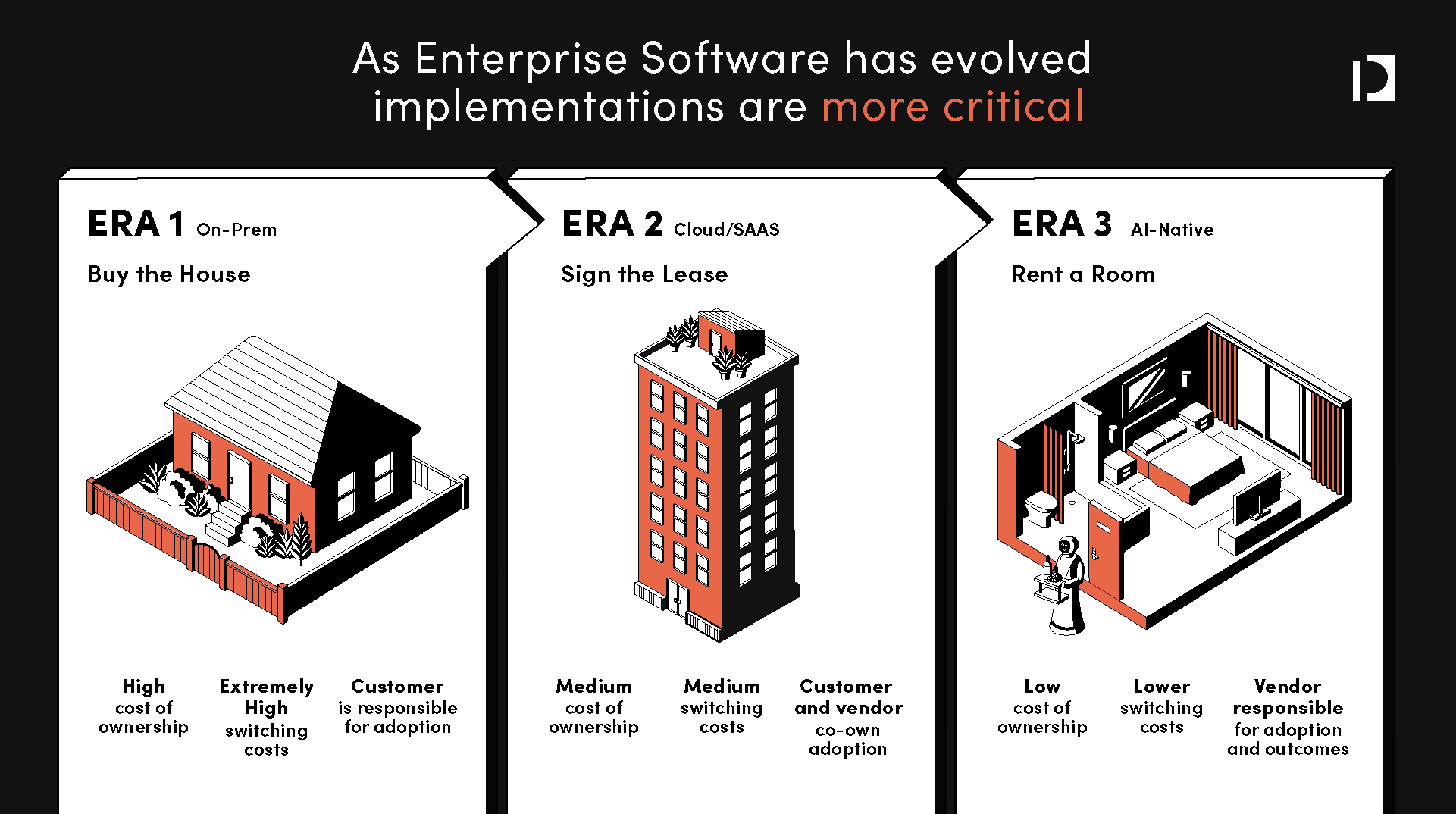

- On-prem (“Buy the House”) - large upfront investment, extremely high switching costs, ongoing monetization through professional services, in-sourcing of customization/implementation

- Cloud/SaaS (“Pay Rent”) - medium upfront investment, medium switching costs, ongoing monetization driven through expansion, outsourcing of implementations

- AI-native (“Hotel Rooms?”) - low cost of ownership, increasingly lower switching costs, ongoing monetization driven by value delivered to the business, high need for proper implementation

The On-Prem Era - “Buy the House”

In the on-prem era, enterprise software functioned much like buying a home outright: customers made a large, upfront license commitment long before any value was realized. Extremely high upfront cost of ownership and on-prem delivery meant that picking any system was a monumental decision. From there, software vendors were both able to and forced to extract ongoing value by charging through the nose to send a team onsite for every upgrade, patch, workflow change, or new integration.

As a result, professional services became a significant revenue line and a structural dependency. The knock on effect was that software had slow improvement cycles, deployments were brittle, and releasing new functionality was expensive and logistically complex. Switching costs were so high that “Customer Success” did not exist as we know it today; rather post-sale engagement centered on “Account Managers”, whose remit was increasing contract value rather than ensuring product outcomes. The guiding principle of the on-prem era was stability and control, not adaptability or continuous value realization.

The Cloud/SaaS Era - “Sign the Lease”

The transition to cloud introduced a fundamentally different software operating model. Instead of owning software outright, customers switched to recurring subscriptions akin to paying rent. Delivery in cloud environments made software improvements effectively free, with vendors shipping updates in the form of new features and functionality directly to customers. Professional services largely moved away from being a consistent, recurring revenue stream (that’s paying for the software instead) and more limited in scope to the “one time” upfront customization and onboarding work needed to adjust an “out of the box” solution to an enterprise customer.

The more one-time nature of the implementation meant that the scaled platforms largely outsourced this work — creating one of the largest services markets in enterprise IT. Global systems integrators (GSIs) emerged as a category – a $550B+ services ecosystem to support SaaS adoption. GSIs today represent nearly ~9% of all global IT spend.

In this era, the growth path for software companies in this era shifted to license / seat growth within accounts. NRR became the north star metric and therefore the optimization of expansion, renewals, and upgrades. This lowered switching costs (relative to the on-prem era) and birthed the “Customer Success” function to professionalize the processes behind account growth.

SaaS improved time-to-market and made product improvements effectively free. The lower cost of ownership meant the average number of SaaS applications per company grew from 8 in 2015 to 130 in 2022. For complex enterprises, value realization still depended on services-heavy, bespoke implementation work. This compounded with complexity as tech stacks broadened through the “unbundling” era of software. In this era, how the product was configured, integrated, and rolled out often determined actual ROI.

Entering the AI-Native Era - “Rent a Room”

In this emerging era, “software” is increasingly shifting to usage/value based models where customers effectively “pay as you go” for the value that they’re consuming.

The risk of a “bad” implementation increases exponentially because:

- Revenue starts at consumption - usage/outcome-based pricing moves revenue recognition and ACV growth to consumption, making implementations the primary bottleneck

- Probabilistic nature of AI requires more testing - non-deterministic output makes continuous evals and tuning critical, and model updates mean today’s functionality cannot be taken for granted tomorrow

- Implementations become a moving target - the combo of rapidly evolving underlying models and customer-side inputs mean implementations are stale almost immediately. “Go-live” becomes the start, not the end, of implementation. In the SaaS era, it was widely accepted that “Phase II” of an implementation oftentimes never happened as customers were so fixated on the exercise of “going live” that they more often than not lost steam on anything further. AI-era buyers will demand more.

- Software adapts to customers, not the other way around - the SaaS era provided opinionated solutions that were largely “take it or leave it”. AI-native solutions need to capture the nuances of tacit knowledge, tone, and culture of the end customer in a way that makes discovery exponentially more complex.

As a result, AI-native app companies today are each reinventing the implementation playbook from scratch. There is no “system of record” that captures customer level configurations and playbooks in a repeatable way. Implementations are increasingly a product problem (in fact – we are seeing an increase in implementation orgs structurally rolling up to the CTO). Companies are throwing bodies at the problem – and they’re expensive ones (in the form of “FDEs” too):

The last generation of customer success software (i.e. Gainsight, Catalyst) was largely a disappointment. The main challenges they faced were 1) mediocre ROI and 2) CS leaders had thin budgets and 3) existing solutions were largely reactive to what happened (oftentimes too late) vs. proactively recommending intervention and 4) data ingestion was massively painful

This is now changing. The AI-era is blurring the line between pre and post sales as we move to a continuous delivery model. In this world, the implementation org is no longer a cost center, they are becoming a core revenue driver.

Early observations in the market suggest:

- Persistently wide CARR > ARR gaps – Anecdotally we are regularly seeing CARR 3-5x higher than live ARR as many AI apps providers enter “land grab mode in an aggressive market”. Strong market pull is no longer the hallmark of PMF given top down AI experimental mandates. Retention is the new bar for PMF. This is shifting implementations from “expensive” problem to board level “hair on fire” priority

- Structurally lower gross margins – 70-80% SaaS margins are a thing of the past. Up to 56% of SaaS vendors now have variable pricing. With unit costs scaling with model usage, poorly tuned systems will become more expensive to deliver (as you have to re-run queries) and lead to weaker gross margins.

- “Implementing” is a continuous state – the underlying models and products are evolving so quickly that implementations are basically out of date as soon as they are complete. As vendors and customers alike are adopting agentic workflows in real time, there needs to be constant communication and adjusting (vs. a customer success team parachuting in right before the contract expires!). Again, this is a stark contrast to the SaaS era, where both buyers and customers became complacent with stale implementations until they reached the point of churn risk.

- GTM teams need new metrics around customer health – GTM teams will rely on new leading indicators of customer health in addition to the tried and true NRR metric. NRR is a lagging indicator of customer health and AI-native companies do not have the luxury to wait it out. Forward-thinking leaders are adopting new metrics to hold themselves accountable to customer value (e.g. Outcome Metrics 1.0) and we expect some of these to become the new normal.

- The right talent to do this is way more expensive – “FDEs” of every kind are en vogue – demand has grown 12x in the past year. Given the product depth, subject matter expertise, and oftentimes technical needs to get these implementations right, this talent is a much more expensive one — roughly 1.5-2x the cost of a typical CS associate. Historically a good implementation manager could manage 8-10 projects at a time; the deeply embedded model is scaling that way down. That’s changing too with 50% more of AI-native GTM teams in post-sales roles (vs. SaaS peers). Add this up and the total cost of implementations skyrockets.

The bottom line is that the onus of ownership is shifting from the customer (in the pre-SaaS world) to now almost entirely on the vendor. Getting in the door is now easy, staying relevant towards actually delivering value is much more difficult.

So What Does this Mean?

For Enterprise AI Apps, the implementation layer is emerging as the true battleground for category leadership. What endures is a vendor’s ability to implement, align, and maintain AI systems in live environments.

So the questions for a company in this space become:

- Is this a point in time problem? It’s still early days and most of the app layer is in “land grab” mode. At a more steady state of market penetration and product maturity, does the severity of the problem change?

- Can it be productized? Each category and even each end customer may require a bit of a different approach. Is there a set of collective primitives that will emerge that allow for repeatability (vs. just becoming a modern systems integrator)?

- Will implementations be “too” mission critical? Is a good implementation too much of the “secret sauce” to the point where each AI-native app company will want to own the process themselves? Anecdotally – we don’t think so. From what we’ve seen, although implementations are a huge problem, companies would rather dedicate limited resources towards core product development.

AI-native companies need to cross a new kind of chasm. The willingness to try is largely there, the willingness to stay is yet to be seen. We believe this dislocation creates a unique “why now” for a new “system of record” that is centered on the existing customer and enables continuous, ongoing implementations to emerge.

There have been a handful of new companies that have emerged to tackle this problem and automate implementations leveraging AI. There’s three main approaches:

- Arm the SIs – companies like Auctor builds tools to help traditional SIs deliver better implementations.

- Replace the SIs – these are tech-enabled services businesses that are focused on replacing the legacy consultants that are brought in to implement heavyweight software systems. Tessera focuses on ERP migrations while Echelon centers around ServiceNow work.

- Augment (and over time automate) internal delivery teams – systems like Axiamatic serve companies going through transformations while Genera supports AI-native companies who have hefty implementations processes.

As last mile delivery of software — in particular agentic software — becomes increasingly critical we know that the “FDE” role is only going to continue to grow in popularity. Implementations are becoming a front office problem and there’s a massive opportunity to help support this delivery problem as we shift into this new era of software consumption.