I. The End of “More for Less”

For decades, digital progress followed a simple promise: more for less. Each new generation of chips delivered greater capability while consuming less power per operation, a relentless march of efficiency initially captured by Koomey’s Law (the observation that the energy efficiency of computation doubles roughly every 1.5 years). That trend continues as silicon chips get more efficient, but its impact has fundamentally changed.

Today, efficiency gains that once reduced energy use are now enabling an explosion in compute demand driven by frontier AI. This dynamic, consistent with Jevons’ Paradox, which states that improvements in efficiency don't conserve a resource, but instead expand total energy consumption by making its use cheaper and more widespread. Everyone agrees we’ll need exponentially more energy to power the AI future. Hyperscalers themselves now openly acknowledge that energy is their single biggest operational constraint. Where and how fast they can deploy AI depends on where they can find power.

The open question is how best to address this bottleneck when gains from hardware and algorithmic efficiency are no longer enough to overcome it. The conventional view from Koomey’s Law focuses narrowly on chips and models. While we appreciate the critical and ongoing work being done in hardware and algorithmic efficiency by many smart individuals (including our colleagues), the constraint we are focused on lies in the broader system-level energy relationship. That is, the full end-to-end energy supply chain of AI from computation to cooling, from data centers to the grid, and from turbines to transmission lines. Meeting this moment will require a complex, multi-layered solution that involves simultaneously improving existing infrastructure, rapidly adding power supply, and deploying new efficiency technologies across the entire system.

The Energy-Intelligence Hypothesis (EIH) provides a framework for understanding that chain and suggests that if we keep shipping model improvements at the projected rate, the demand for compute will outpace advancements in the physical infrastructure required to power it. That infrastructure will also often be built inefficiently, compounding the problem over time.

There may even be a measurable, testable relationship between intelligence and system level energy consumption. The same way there are scaling laws that exist between model loss and compute, there might be something similar between AI model capability and system-level energy consumption. For now that’s above our pay grade, but the evidence we see in the market suggests there is a diminishing margin of return on energy in the AI race.

The goal of our framework is to explore how energy constrains AI progress. We decompose total system energy into four measurable subcomponents of 1) compute-level, 2) data-center-level, 3) grid-level, and 4) power-plant-level energy to identify where the system is bottlenecked and why.

The scale of this challenge is defined by a fundamental structural mismatch: exponential compute demand is mathematically driven by the scaling of frontier models, but the physical energy infrastructure (power plants, transformers, and transmission lines) is characterized by slow, multi-decade capital expenditure cycles, lacking the agility to respond to digital-age velocity. This misalignment is exacerbated by history. Energy systems are traditionally structured to meet growth primarily through efficiency gains (historically, efficiency gains have contributed more to energy growth than new supply). However, the US electricity demand was largely flat for over twenty years, meaning the sector lacks the institutional "muscle" and streamlined supply chains needed to pivot from slow efficiency gains to massive, rapid physical expansion. The urgent need to grow data center energy capacity from 17 GW today to over 130 GW by 2030 requires a new playbook.

II. From Chips to Systems: The EIH Framework

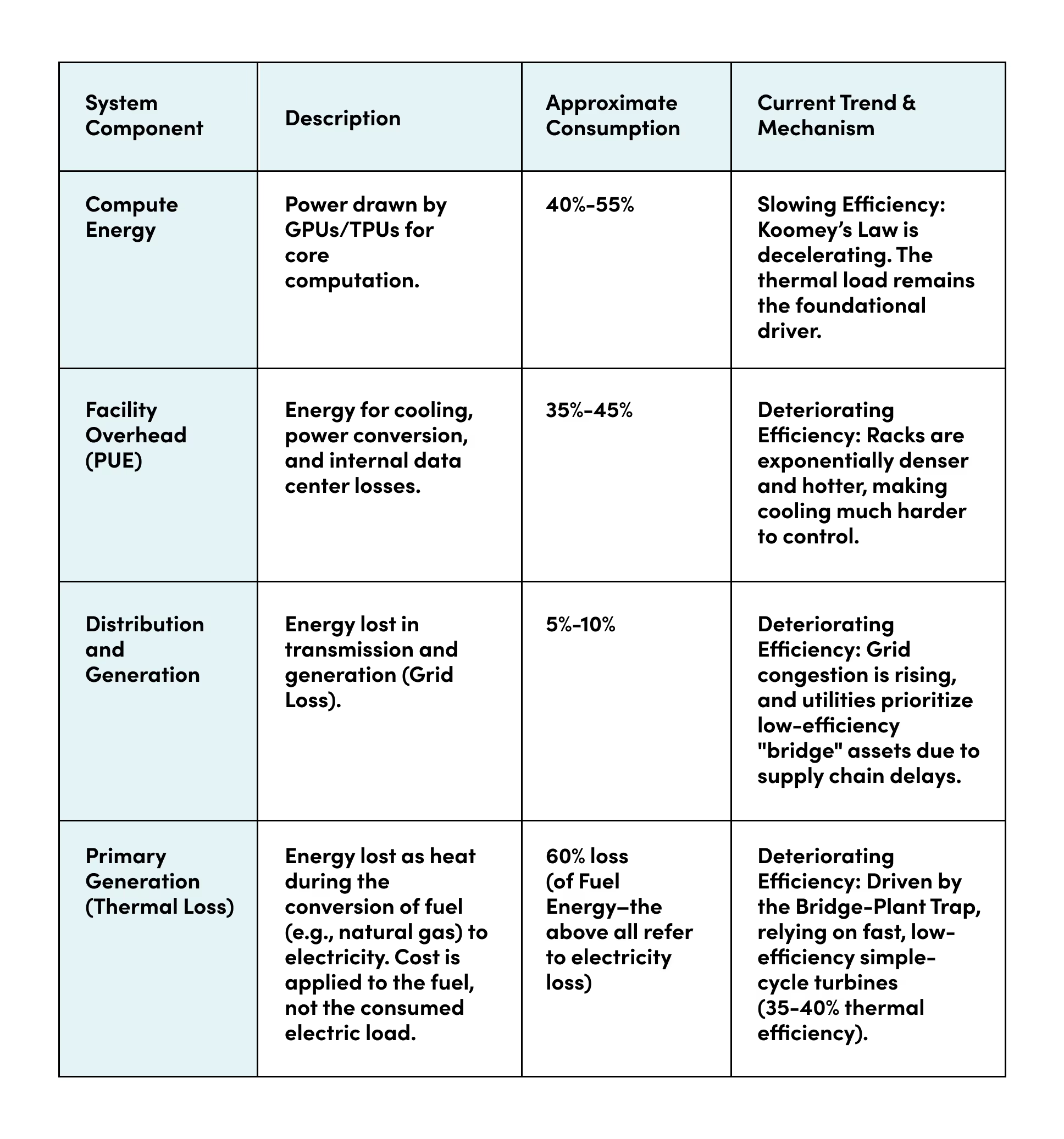

The traditional lens of compute’s energy efficiency zoomed in on chips and models. The landmark KPI of the AI economy has been tokens per watt, which clearly ties compute to energy, but not beyond the GPU level. It doesn’t include the entire supply chain of energy that was lost in the delivery of electrons to the GPU. We think the frontier of constraint has moved. The modern AI stack is no longer just about software and silicon. It’s now a physical infrastructure system.

Understanding this requires shifting from chip-level efficiency to system-level energy, encompassing the full physical chain that delivers usable power to computation. That system can be broken into three interacting layers that combine to define the total energy required by a massive AI deployment.

Deteriorating Efficiency: Driven by the Bridge-Plant Trap, relying on fast, low-efficiency simple-cycle turbines (35-40% thermal efficiency).

The lesson is clear: The marginal efficiency gains from the chip are not enough to overwhelm the compounding losses across the rest of the energy supply chain. Chips and algorithms are only half of the problem. The solution requires looking at the rest of the system as rigorously as we have looked at algorithms and chips.

The energy economy of AI has entered what might be called a System-Level Rebound, where efficiency at the compute level drives inefficiency at the energy system level. The signs of the demand spike and its impact on the system are plain to see:

- Demand Shock: U.S. data-center demand of 17 GW in 2023 is projected to exceed 130 GW by 2030, requiring the buildout of more than 100 new large power plants in seven years.

- Speed Over Optimization: Hyperscalers now prioritize speed to power over cost or sustainability. Interconnection queues have ballooned by over 200% year-on-year.

- Structural Capex Lock-In: Every short-term fix (extra transformers, emergency aeroderivative turbines, ad hoc cooling) becomes long-term infrastructure. Once built, inefficiency calcifies, guaranteeing that total system energy continues to scale exponentially with compute, even as individual components become more efficient.

The rebound ensures that the constraints from cooling, distribution, and generation will overwhelm the dwindling efficiency gains from hardware and algorithms. The suddenness of this demand shock is made more poignant by how stagnant energy growth was in the decades leading up to the AI buildout. The system is structurally unprepared for this non-linear acceleration

IV. The Evidence of Systemic Slowdown

The systemic buffer that once kept compute sustainable is collapsing under pressure from four measurable factors:

1. Hardware Efficiency: Koomey’s Law is Losing Momentum

The legendary Koomey’s Law (computational efficiency doubling every 1.5 years) has flattened dramatically since 2015. Today, the doubling time for computational energy efficiency has slowed to around 2.3 years. This is primarily attributed to the end of Dennard Scaling, a decades-long trend that allowed manufacturers to increase transistor density without a proportional increase in power. This deceleration is not temporary and is constrained by fundamental thermodynamic principles (like the Landauer limit) that determine the absolute minimum energy required to compute. This points toward the eventual end of these gains.

2. Facility Efficiency: The PUE Plateau

Power Usage Effectiveness (PUE), the industry’s metric for data-center efficiency (Total Facility Energy/Compute Energy), tells a story of rapid initial success followed by painful stagnation. Pre-cloud data centers operated with PUEs near 2.0 (meaning 1 Watt wasted for every 1 Watt used for compute). The cloud boom drove this down sharply to a best-in-class average of 1.2 by 2018.

Today, however, PUE has stalled globally around 1.6. This failure to improve is not benign: as chip density rises, the cooling challenge has changed from a linear problem to an exponential one, with internal losses from cooling and power conversion eating a larger share of energy. GPUs optimized for AI deliver enormous performance, but are becoming hotter and hotter engines. Nvidia’s H100 draws up to 700 watts; high-density data-center racks now exceed 100 kW, with projections nearing 1 MW by 2030. The implication for the AI buildout is catastrophic. If the industry achieves its projected 130 GW IT load by 2030, the PUE plateau at 1.6 means the industry will waste over 52 GW of power on cooling and overhead (78 GW total overhead at PUE 1.6 vs. 26 GW overhead at PUE 1.2). To put that in perspective, the 78 GW of total overhead power capacity required just for cooling and conversion is roughly equivalent to the peak summer electricity demand of the entire state of Texas.

3. Transmission & Distribution: Losses that Don’t Shrink

The physical process of moving power from the plant to the plug is inherently inefficient, typically resulting in 5-6% of all U.S. electricity disappearing in transit. Grid loss is directly impacted by distance, density, and critically, the quality and age of equipment (substations, transformers).

Today, the AI buildout is actively pushing this loss rate higher. Despite efforts to move behind-the-meter, the concentrated, high-density demand from hyperscalers is immediately exacerbating local grid congestion. This rising congestion increases current flows across existing infrastructure, which consequently drives up thermal losses within the aging system. Moreover, the massive supply chain bottleneck for critical, high-efficiency components like Large Power Transformers (LPTs) (most major suppliers have four-year backlogs) forces utilities and IPPs to patch the system with refurbished or older, lower-efficiency hardware to meet deadlines. This strategic necessity sacrifices long-term efficiency for short-term speed to meet urgent near-term AI demand. We believe this will cement longer term systemic inefficiency into the grid itself.

4. Generation Efficiency: The Bridge-Plant Trap

To meet surging, immediate AI demand, power providers are forced away from optimal, high-efficiency solutions like Combined Cycle Gas Turbines (CCGT), which face five-year backlogs and supply chain bottlenecks (discussed in detail in our last newsletter). Instead they are using faster-to-deploy, lower-efficiency options like aeroderivative turbines or refurbished simple-cycle gas units. These assets are thermally inefficient (35-40% efficiency) compared with CCGTs (55–60%). This short-term scramble for capacity locks in lower efficiency, higher emissions, and higher future costs over a power asset’s multi-decade lifespan.

V. Strategic Implications: The New Investment Thesis

Behind every token is a stack of software, hardware, and physical energy infrastructure, the latter of which is being strained to its limits by compounding token growth. We must address the physical layer head-on. We highlight four immediate strategic shifts necessary for investors and founders to manage this new reality, which we believe offer significant opportunities for new companies. (This is admittedly high level, and we will dive deeper into each of these in subsequent newsletter posts). The strategic shifts outlined below focus exclusively on the physical energy chain and do not address the essential, ongoing work in chip and model efficiency.

1. High-Velocity Supply Buildout

The AI demand shock requires the power sector to pivot from slow, multi-decade planning to rapid, industrial-scale deployment. This category focuses on accelerating the speed and efficiency of deploying new power and transmission assets.

- Infrastructure Bypass Solutions: Developing pre-fabricated modular power solutions, solid-state transformers, and advanced utility-scale batteries to circumvent supply chain bottlenecks for critical grid components.

- Supply Chain Investment: Investing in the manufacturing capacity for critical power infrastructure components (e.g., turbine blades, generators, transformers) and securing supply chains for key materials (e.g., lithium, copper, and rare earth minerals).

- Grid Modernization & Optimization: Creating durable power electronics and grid-enhancing technologies (GETs) that improve the flexibility, reliability, and capacity of existing transmission lines, enabling faster interconnection for new generation.

- Power Infrastructure Enablement: Investing in technologies and processes that enable grid infrastructure and power plants to be built faster and more efficiently, often using standardized or modular designs.

2. Data Center Facility Resilience

This focus area tackles the data center's most immediate physical challenge: heat management and maximizing the utility of every electron. These solutions improve data center efficiency and ensure BTM assets contribute to local stability.

- Thermal Management: Investment in solutions like liquid immersion and direct-to-chip cooling, and high-efficiency UPS/PDUs to stabilize facility overhead (PUE) against rising chip density. There are also “extreme” thermal management companies focused on building data centers in environments that are less susceptible to heat constraints (underwater, space, etc).

- Stranded Energy Recapture: Focus on heat exchangers and campus-integrated cooling systems to convert waste heat into reusable energy, maximizing thermodynamic efficiency.

- On-Site Flexibility: Solutions that enable data center batteries and BTM generation to provide localized resiliency and participate in demand flexibility programs.

3. Frontier Energy Supply & Bypass

To meet long-term energy needs beyond what traditional generation can provide, investment must flow into new, high-capacity, firm, and decentralized sources. These are the "deep tech" solutions that radically increase available supply.

- New BTM Generation: Scaling Behind-the-Meter (BTM) co-located generation technologies like modular nuclear, advanced geothermal, and long-duration storage (LDES) to bypass grid congestion and delivery loss.

- Energy-Agnostic Sites: Developing power-agnostic data center designs that can quickly integrate non-traditional, firm power sources, accelerating the speed-to-market for new supply.

4. Digital Infrastructure: Planning, Visibility, and Flexibility

This category focuses on integrating software and data to solve the system's structural planning and efficiency challenges, benefiting both grid operators and data center developers.

- Grid Infrastructure Data Solutions: Companies that provide high-granularity, node-level data mapping and competition analysis of grid capacity, interconnection queues, and future power prices. This is critical for optimal data center siting and project financing (e.g., replacing manual transmission studies with data products).

- Predictive Resilience: Software tools, including advanced Load Management Systems (LMS) for utilities, that use AI to forecast demand, predict grid downtime, and optimize transmission flows, enabling proactive control and reducing system losses.

- Intelligent Load Management & VPPs: Energy-aware schedulers that enable temporal routing, aligning compute demand with instantaneous energy supply and price. This includes platforms that turn large, schedulable AI load into a valuable grid asset by developing Virtual Power Plants (VPPs) that aggregate flexible load and enable BTM capacity to actively export surplus power back to the utility.

In our next issues we’ll break down each of the four opportunity areas outlined above. As always, if you are receiving this it means we respect your opinion and encourage your feedback. If you have any thoughts or are working on solutions to the problems we discussed, we’d love to hear from you.