.avif)

Pros and pitfalls we’ve noticed in the emerging category

“Vertical AI” is one of the buzziest categories in early stage investing. That’s for good reason, with early breakouts including Abridge and EvenUp raising a collective $570 million in 2024. These companies share a similar premise: Do work rather than facilitate work, therefore capturing services spend (13% of GDP), rather than software spend (1% of GDP).

While it’s easy to view Vertical AI companies as the natural evolution of Vertical SaaS in the age of LLMs, we believe that they are fundamentally different from their predecessors. Specifically, Vertical SaaS companies were SaaS companies; vertical AI companies come in multiple different forms, some of which are not pure SaaS. As such, founders need to carefully evaluate which business model is optimal for each market when launching a Vertical AI startup because the business model will inform some of the key risks and core advantages.

What are the categories of vertical AI companies?

Vertical AI companies have a slew of different options when it comes to choosing a business model. With that said, nearly all of these businesses are doing one of two things: they either enable a service provider or are a service provider. There are multiple different business models in both categories.

Each of these categories have distinct advantages and disadvantages. In this article we’ll give an overview of how we evaluate each.

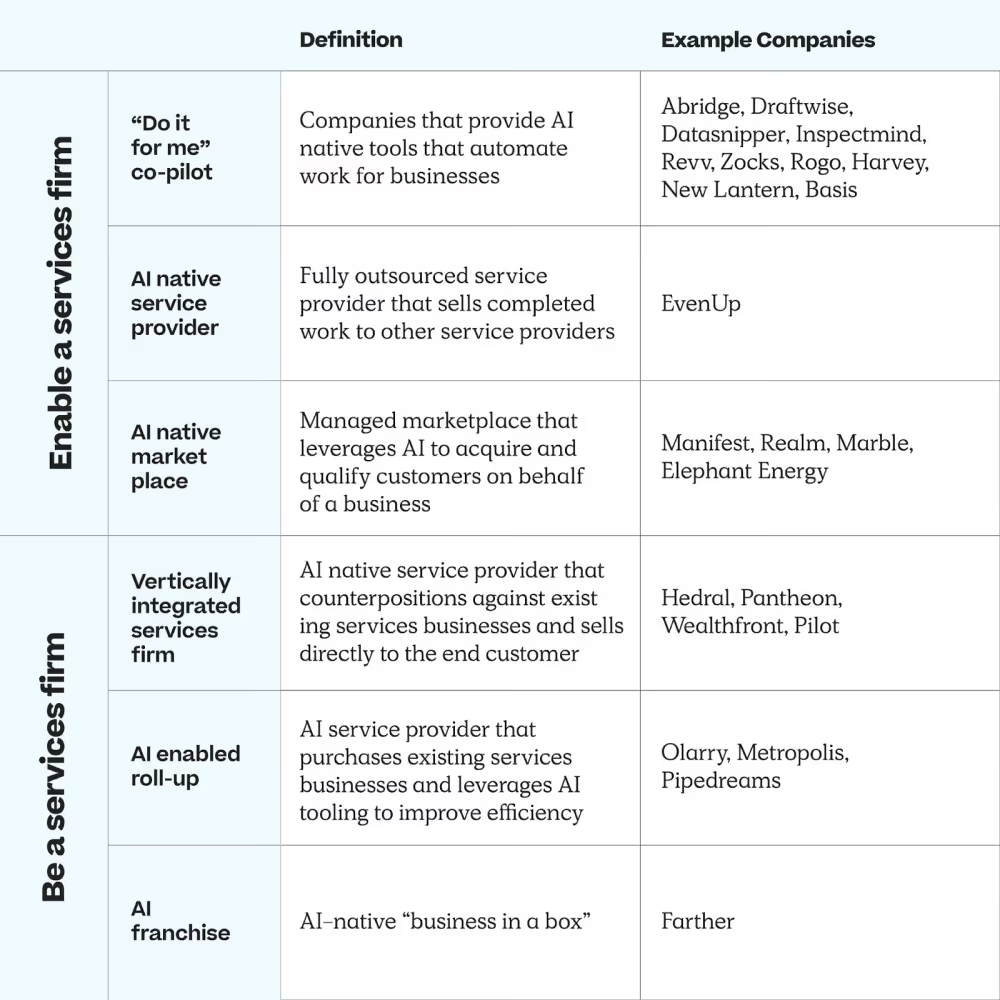

Enabling Service Providers

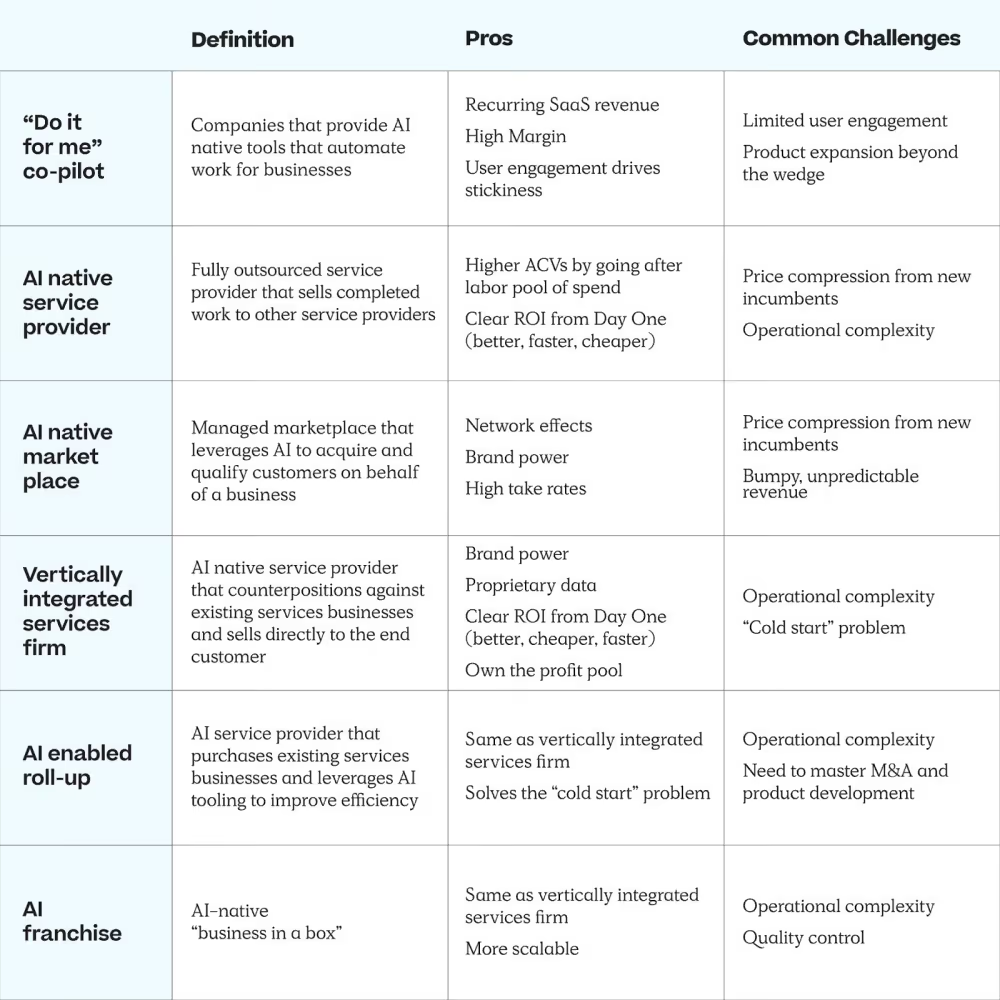

“Do it for me” co-pilot

The AI co-pilot is the most popular business model we are seeing early stage vertical AI companies pursue today. These companies have all the advantages of traditional software businesses: high margin, recurring revenue, sticky (ideally), with seemingly easier sales cycles than their vertical software predecessors.

Co-pilots are especially attractive for companies that serve SMB and SME customers, as the breakouts offer a significantly improved ROI compared to traditional vertical software. These companies are growing quickly by automating work rather than providing incremental productivity gains via workflow tooling. Oftentimes with incredibly fast or immediate time to value. We’ve written extensively about this theme in our SMB Tech Installment of Change Order.

On the other hand, co-pilot business models come with their own set of challenges. We’ve seen these business models have two major challenges:

1. User adoption: Co-pilots that require a significant customer behavior change will likely struggle to drive user adoption. We’ve seen the most hesitancy around two themes:

2. Product expansion beyond the wedge: We believe that there will be a massive number of successful wedge products that plug into the system of record and quickly grow to $50m+ ARR. At the same time, we have questions about how many of these companies will go on to become enduring generational businesses.

Reason to Win: The ones that do will have won because the founder determined the second act early into the company life cycle (ideally months or even weeks into launching the wedge product) and had a magical experience for end users from day 1. The profit pool or labor spend that you go after with your second act should dictate your pricing strategy and engineering resource allocation to determine the speed at which you should attack that second act.

Key Risk: The fundamental risk of meeting customers where they already work is that the system of record company can complicate or even turn off existing integrations. They can also launch their own version of your tool. If the end goal is to replace the core workflows of the system of record, vertical AI founders must be extremely clever and move fast in launching new products.

AI Native Service Provider to Other Service Providers

Companies like EvenUp have averted a core challenge of the co-pilot model—end user adoption. They’ve done this by becoming an outsourced service provider and selling work to the services firm, rather than selling software. These companies typically go after the labor pool of spend rather than software budgets. EvenUp, for example, prices as a percentage of a law firm’s existing paralegal staff. Consequently, they are able to drive larger ACVs from Day One, enabling them to grow revenue quickly.

Unlike many co-pilot solutions, service providers often go after enterprise customers first. This is because enterprise customers own a disproportionate percentage of industry data, which is critical for building an early data moat and offering a 10x better service as you go down market.

While these companies can grow fast, they also have two core challenges:

1. Pricing pressure from new entrants: Skeptics say the question surrounding AI native service providers like EvenUp is a lack of defensibility within their wedge product. While locking up enterprise customers and leveraging their data to build a better product gives these companies a strong first mover advantage, we don’t believe that is the sufficient driver of long-term defensibility.

The enduring service providers will have to find ways to build defensibility in their second act. If they don’t, they are likely to be undercut on price by new entrants and ultimately suffer from thin margins driven by downward pricing pressure.

2. Operational complexity: Leveraging AI to build a services business does not negate the fact that it is still a tech-enabled service and may face many of the same challenges that services businesses have always faced. One obvious operational pitfall is lumpy, project-based revenue tied to market cycles. This creates two core issues: The first is around staffing utilization, which when sub-optimized can pull down gross margins; the second is around building a recurring, predictable revenue stream that will be valued at a higher multiple. To date, we’ve found that the best way to drive more predictable revenue is by charging a minimum spend upfront or using a credits-based system.

Ultimately, these companies will need to be very thoughtful in how they manage their “human in the loop” workforce and set up the right data infrastructure to enable their workforce to train the AI models over time.

Reason to win: AI native service providers selling to other service providers should be able to capture more gross profit dollars per a customer than their purely software peers. They should also find acquiring customers a bit easier than software tools as the change management problems they experience from an operational perspective is likely much lower than pure software, especially if their service provider customers already have a budget for outsourcing the specific activity.

AI-Native Marketplace

An often overlooked business model in the Vertical AI landscape is AI-native marketplaces. Once a hot business model in the early 2010s, marketplace investors have struggled to find true breakouts in recent years. Most of the large markets had been won by the time customer acquisition costs leveraging online marketing started to rise. We’re now entering an era where marketplaces can thrive again as AI fundamentally shifts the cost structure in some categories that were deemed too challenging prior.

This business model is relatively less common, though we’ve seen a couple take off and grow very quickly in the legal sector, including Manifest and Marble. Both of these companies are going after micro-SMB or solopreneur law firms who do not have the bandwidth or marketing muscle to spend significant time on customer acquisition.

These businesses leverage AI for customer acquisition, as well as customer success on the demand side and automation of work on the supply side.

By delivering a fully vetted customer (not a lead) and automating much of the low hanging fruit involved in servicing that customer through AI, these companies are able to command high take rates on each “job” they deliver and provide end consumers with a “better, faster, cheaper” option. They’re able to do so because AI enables two important efficiency gains:

- Each of the marketplace’s sales rep and CX agent can handle 10X the amount of customers they were able to before

- Each service provider on the other side (i.e., the law firm) can take on more clients as traditionally manual tasks are automated away with AI

Another key insight that will lead to very strong AI-Native marketplaces is strong cash conversion cycle dynamics. Markets in which the marketplace can collect revenue on day 1, but not pay out the service provider until day 30-90, creates incredible dynamics whereby the company can reinvest the dollars into growth. Consequently they are able to grow very quickly.

In addition, marketplaces have an innate network effect built into their business model. They can also start building strong consumer brands through a high-quality customer service experience and transparent pricing. While these companies can be harder to scale as founders need to acquire both supply and demand, they’re inherently more defensible.

With that said, they come with their own set of challenges:

1. Price compression from new entrants: Similar to vertically integrated service providers, as these AI-native marketplaces start to truly take off, new players will enter the market. While marketplaces benefit from strong network effects, we believe that new entrants might drive up customer acquisition costs and put downward pressure on pricing. The 50%+ take rates we see today are likely not sustainable long term.

2. Bumpy, unpredictable revenue: Depending on the type of service, transactional revenue is typically not as predictable or valuable in the public markets as SaaS revenue. These companies will need to scale to much larger sizes to achieve similar valuations to their SaaS counterparts. The good news is that many of these markets are absolutely massive and represent strong wedges into more recurring revenue streams based on the building of trust with their end consumers (e.g. financial advisors making recommendations for annuities, insurance, etc.). It’s critical for founders to build in marketplaces where there is still a venture scale TAM opportunity even with pricing pressure.

Being a Service Provider

Vertically Integrated Services Firm

Unlike AI Native Service Providers, Vertically Integrated Services Firms are not selling discrete work to an existing service provider. In contrast, they are disrupting that service provider by offering an often cheaper, faster, and/or better experience to the end customer. They are able to do this by leveraging AI to automate away some traditionally manual, time consuming, and expensive processes that are done by humans today.

On the surface, AI Native Service Providers and Vertically Integrated Services Firms share many of the same advantages and disadvantages. However there are critical tradeoffs between being a services firm and enabling them.

Advantages of being a services firm no matter how you do it:

- Owing the profit pool: By being the services firm, businesses own the entire profit pool. You have more control over the core drivers of profitability and can experiment with different tooling to drive costs down over time.

- Capture and create truly complex and proprietary data: Vertically integrated services providers typically develop nuanced understanding of complex processes by having access to significantly more data than either type of Vertical AI business. With proprietary data comes key insights that typically lead to a higher level of automation and a more delightful customer experience over time, all of which are likely to drive true first mover advantages.

- Brand power: By offering a better service directly to end customers, these companies can build durable and lasting brands that users associate with a high trust experience and a quality product.

- Rethinking the end customer experience and internal operations from the ground up: Launching a new services firm means you get to reimagine firm operations and the customer experience. If a services firm charges customers on an hourly basis today, they’re not incentivized in most markets to leverage AI to become more efficient as it’ll impact their topline. When building a new firm, you could easily rewrite the rules and charge on a project basis. Additionally, legacy firms are stuck with old clunky software tools that they’ll likely struggle to replace and sub-optimal processes for their end customer. By launching a firm from scratch, you can fully reimagine operations and pass a lot of that value onto the end customer.

There is a core disadvantage:

- Operational complexity: Being a service provider is fundamentally more operationally complex than enabling an existing firm, especially on the onset. It takes an incredible amount of high quality hiring, process development, and industry expertise. Consequently, the capital requirements are often very high.

- Exit Multiples: Services firms have historically traded at lower multiples than software companies. This may impact a startups valuation in both the private and public markets, as well as deter some downstream investors from wanting to get involved.

Ultimately, founders need to weigh operational complexity with the possibility for larger profit pools and a stronger moat when choosing between becoming a services firm and enabling a services firm.

AI Enabled Roll Up

In order to avoid the cold start problem, some founders may consider purchasing an existing services firm and layering on AI tools in order to deliver a better, faster, and cheaper service. These companies are essentially a Vertically Integrated Service Provider but their core advantage is that they are skirting some of the operational complexity involved with starting a services business from scratch. They do not have to worry about hiring every employee and setting up all new systems; and immediately have access to a wealth of data. Most critically, they are starting with a book of business and from a place of trust with existing customers, which is critical in relationship driven industries like accounting.

They have one core disadvantage compared to Vertically Integrated Service Providers that are starting from scratch:

- They need to master M&A and product simultaneously: While this may seem like an issue that can be solved with the right talent, M&A and product are two very important yet very different core competencies. It’s rare for a founding team to have both. Consequently, many of these businesses may end up looking more like private equity roll-ups than a tech enabled services firm. On the other hand, the team may build great products but acquire bad assets. Either way presents a challenging path ahead.

- Change management: Acquiring an existing business means inheriting existing talent, culture, and ways of working. Large companies often hire slews of outside consultants to enact change management. While the process is usually simpler at smaller organizations, it is still likely to be challenging and time consuming, especially when it comes to digitizing traditional tech laggard industries.

AI Franchise

A third flavor or “being a services firm” is becoming an AI franchise. These founders recognize the operational complexity of building a services firm and instead of trying to scale on their own, they leverage the power of their tooling and brand to drive growth. The core advantage of this approach is scalability and capital efficiency. It’s easier to offload some of the growth and management to entrepreneurs who have expertise in their own markets. Additionally, it’s incredibly powerful in markets where the franchisee takes on some initial capex investments (e.g. robotics or other equipment) vs. the franchisor startup itself. In many instances AI franchises will have higher ACVs than pure SaaS companies selling to the same target customer base if you assume that their “franchise fee” is in line with the franchise royalty rates of today.

However, that same advantage comes with one core disadvantage:

- Quality control: It will be harder for entrepreneurs pursuing this approach to ensure that their brand power does not get eroded over time by sloppy operators. Having strong compliance mechanisms in place and a thorough onboarding process is critical for the success of AI franchises.

While these business models have their own unique challenges, we believe there will be multiple generational businesses built in each of these categories.

Founders who find the right business model market fit and nail their second act early in their company’s journey are poised to win. If you’re ideating or building in Vertical AI, please let us know. We’d love to chat with you!

Vertical AI business model overview